45Q Sequestration Tax Credits: Boost for CCS Technologies

Tucked in amongst a host of energy credits in the February Congressional Budget deal were several changes to the existing 45Q federal tax credits for carbon capture and sequestration (CCS) aimed at making the technology more economical. CCS has the potential to be revolutionary for the power sector, once regulatory hurdles are overcome and the technology becomes affordable to scale-up across fossil fuel emitting power plants. These changes to the 45Q tax credits might just be a significant step towards that goal.

What is CCS?

CCS encompasses a host of technologies and methods to capture the carbon dioxide (CO2) emitted during a variety of activities (e.g., fracking for oil and gas, burning coal and gas for electricity, and industrial activities like ethanol production). Instead of having the harmful CO2 be released into the atmosphere, CCS technologies capture and compress the CO2 into a dense gas or liquid that can be transported and used for enhanced oil recovery (EOR) or permanently stored in underground geological structures. While CCS technologies are relatively expensive, they have the potential to reduce CO2 emissions from the atmosphere while providing a reliable source of CO2 for EOR activities.

Tracking CCS penetration in the United States

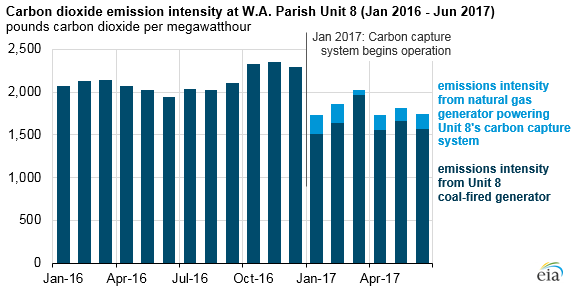

In recent history, CCS projects have struggled to get off the ground. For example, Mississippi Power and Southern Company shut down their proposed CCS project at Kemper Plant due to the project being over budget and behind schedule, a setback to the CCS industry as a whole. On the other hand, the Petra Nova plant, which added CCS to an existing coal-fired plant, was successful in opening on time and on budget, and the plant’s captured CO2 provides an additional revenue stream while boosting oil production at a nearby oil field. In fact, the Petra Nova facility is the only power plant with CCS in the United States and one of only two such plants in the world (with the other being just across the border of North Dakota in Canada), though there are currently 15 large-scale CCS projects in the industrial sector. As data from the Energy Information Administration shows, the Petra Nova plant saw immediate reductions in the facility’s CO2 emissions once CCS began:

As a technology, CCS has generated a fair share of controversy, with one side of experts advocating that its proper implementation is key to any strategy for a decarbonized energy sector, while some environmentalists argue that, even with CCS, the burning of fossil fuels is still more carbon emissive and damaging to the climate than alternative sources of energy like solar, wind, or nuclear. In the end, though, CCS provides another option for reducing CO2 output while providing critical baseload generation.

45Q tax credits and recent changes

In 2009, Congress enacted a CO2 sequestration tax policy aimed at allowing CO2 capture to gain a foothold in the United States. This policy, referred to as 45Q tax credits, provides CCS projects tax credits from the government under the following conditions:

- $20 per metric ton of qualified CO2 that was captured at a qualified facility and secured in geological storage;

- $10 per metric ton of qualified CO2 that was captured at a qualified facility and used as an injectant in a qualified enhanced oil or natural gas recovery project; and

- The amount of credits earned was subject to a maximum of 75 million metric tons of CO2 per year.

The goal of these credits was to provide a financial incentive to integrating the CCS technology, rewarding the power plants who decided to take on the risk of being an early adopter of the technology. The eventual goal is to allow development such that the technology is economical enough to stand on its own and not require policy to continue to support it.

Further, the development of CCS in the United States would likely allow the technology to be more viable for integration in other countries. Not only would such progress be a boon to the companies behind the CCS technology, but it would also bolster the export market for coal to nations that are more slowly transitioning to other power sources and support the coal production industry that is currently watching the U.S. appetite for coal dwindle.

The Congressional Budget deal passed in February 2018 took the 45Q tax credits a step further by expanding the amount of tax credits available to CCS projects that begin construction before 2024, specifically the following:

- Increases the credit for CO2 stored underground from $20 to $50/metric ton (a 150% increase);

- Increases the credit for CO2 used in enhanced oil or natural gas recovery from $10 to $35/metric ton (a 250% increase); and

- Removes the cap on the amount of credits that could be earned in a year and allows qualifying facilities to collect tax credits for up to 12 years.

What does this mean moving forward?

These tax credit increases are particularly valuable to the CCS industry because the United States does not currently tax carbon emissions, meaning there is no negative financial consequence to producing energy or industrial products with a process heavy in CO2 emissions. That being the case, beyond environmental concerns or public image issues, fossil fuel companies had no financial incentive to capture and store their CO2 emissions. The increased 45Q tax credits change the equation, as capturing and storing CO2 now has the potential to bolster a company’s bottom line. This new financial incentive can be an effective way to compel companies to invest in CCS technology while it’s still emerging and somewhat expensive, and thus more risky than more conventional generating technologies.

Not only do these expansions to the 45Q tax credits make the individual decision for a power plant or industrial site to invest in CCS easier, but those individual decisions will likely have a cascading effect of advancing the technology along a learning curve. As more CCS projects are implemented, the cost barriers to CCS will drop and allow more companies the opportunity to invest.

Even in the short time since the expansion to the 45Q tax credits, the industry has seen evidence that CCS will succeed because of these changes. As a former official with the Department of Energy’s Office of Fossil Energy noted, “These changes to the tax code and the enhancements of the 45Q tax credit will absolutely make the difference between a whole bunch of projects being financed and a whole bunch of projects not making it.” With 20 CCS projects currently in development, the future looks bright, but 45Q credits will help improve the economic viability of this technology and will provide utilities with another option for reducing CO2 emissions.

Contact us to learn about how OnLocation can help you explore issues related to energy, CO2 emissions, and how to make the most of 45Q tax credits.