AEO 2025 Trends: Powering Future Demand

Policy Insights Gained from Administration Priorities

The long-awaited release of the U.S. Energy Information Administration’s Annual Energy Outlook (AEO) 2025 in April provides an important benchmark of U.S. energy system projections for various government agencies, research institutions, and industry leaders. These projections rely on the National Energy Modeling System (NEMS), a U.S. energy-economic model that is an industry standard with detailed data and representation of energy markets, policies, and technologies in all energy supply and demand sectors.

This year’s AEO release includes many useful tables of model results but little narrative to help policymakers navigate and interpret the results. In response, OnLocation is launching its weekly “AEO 2025 Trends” blog series that will highlight key results and insights which our experts have gained from the latest AEO scenarios. OnLocation has decades of experience in the application and enhancement of NEMS for its clients and can offer a unique perspective for interpreting the AEO results. This blog is the first in this series, following our initial AEO 2025 overview blog posted soon after the AEO release in April.

EIA’s release includes the AEO 2025 Reference case which projects what the energy system could look like if U.S. laws and regulations in effect as of December 2024 remain the same through 2050. EIA also published two timely AEO 2025 policy-related side cases in addition to the standard side cases produced in prior years: Alternative Electricity and Alternative Transportation. The Alternative Electricity case removes the impact of the U.S. Environmental Protection Agency (EPA) Clean Air Act Section 111 greenhouse gas regulations for fossil fuel-fired power plants, while the Alternative Transportation case assumes several recent regulations, including the National Highway Traffic Safety Administration Corporate Average Fuel Economy Standards and the EPA Multi-Pollutant Emissions Standards for vehicles, are no longer in place. The Trump Administration is in the process of rolling back these regulations to remove impediments to growth of fossil fuel consumption and domestic production.

This article focuses on the results of the AEO Alternative Electricity case and how the power sector results differ from the Reference case. We also compare these results to our recent Energy Horizons (EH) Alternative Policies case that OnLocation developed using our enhanced version of NEMS. The Energy Horizons case projects significant growth in data center energy demand and accounts for new Administration energy policy priorities, including the removal of both the EPA Section 111 regulations for power plants and the Inflation Reduction Act (IRA) Clean Electricity Tax Credits for renewable generation. Congress is considering a phase-out of these credits as part of its latest budget reconciliation bill.

In 2024, in the absence of EIA publishing an updated AEO, OnLocation established its Energy Horizons Series including U.S. Energy System Projections to 2050 and an advanced analysis on Data Center Growth & Impacts on the U.S. Energy Sector.

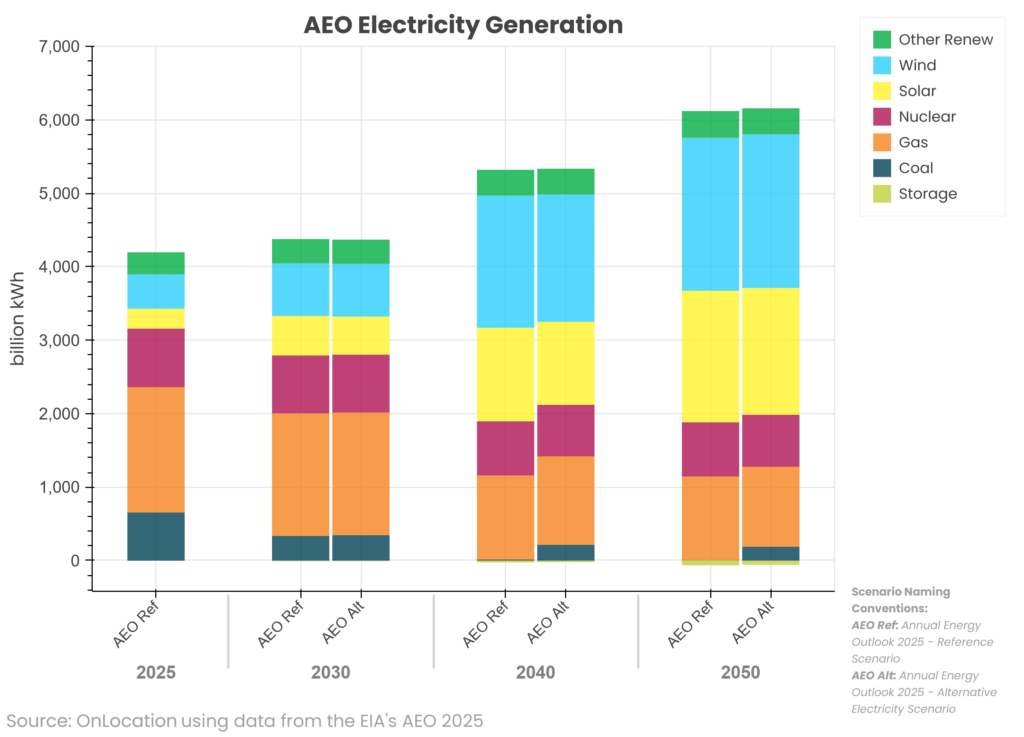

The following chart illustrates the differences in generation mix between the AEO Reference and AEO Alternative Electricity cases. The generation mix in both cases includes fossil fuels (coal and natural gas), renewable energy, and nuclear power. Both cases project substantial growth in total generation, primarily due to the growth in demand from data centers as well as economy-wide electrification trends such as greater adoption of electric vehicles and increased use of electric home devices. In the AEO Reference case, the share of renewable energy, especially wind and solar generation, expands significantly over time, especially after 2030, as the share of fossil energy declines due to EPA 111 regulations for both coal and natural gas. Coal units without carbon capture retire by 2040 as required by the EPA regulations. In contrast, many coal units in the AEO Alternative Electricity case do not retire in the absence of EPA regulations and continue to operate, and total fossil generation (coal and gas) is higher compared to the AEO Ref case, albeit at a lower level after 2030. By 2050, the remaining coal generation in the AEO Alt case displaces some renewable (especially solar) and natural gas generation compared to the AEO Ref case, but renewable generation continues to rise in both cases over time with help from the IRA tax credits and technology improvements that lower the cost of these technologies.

But what if the tax credits for renewables were no longer available?

How much would this policy change affect the generation mix for both renewables and fossil fuels? Comparing the AEO Alternative case with OnLocation’s EH Alternative Data Center case helps paint the picture. In addition to removing the EPA 111 requirements similar to the AEO Alt case, the EH Alt case also removes the IRA tax credits for renewables. While the EH Alt case also has more generation due to an assumed higher growth rate for data center electricity demand than the AEO Alt case, the treatment of the IRA credits is the key driver of the generation differences between the two cases, as shown in the following chart. The comparison illustrates that the generation mix shifts toward more natural gas generation and less renewable generation, especially wind, over time. By 2050, gas generation is 75% higher and renewable generation is 4% lower in the EH case compared to the AEO case. These results suggest that renewable generation will continue to grow without the IRA tax incentives but more slowly, and natural gas will continue to be an important source of electricity in the future.

It is important to note that in all three scenarios, rising electricity demand is mostly met by new natural gas and renewables, especially solar and wind. By 2050, renewables account for 60% to 70% of total generation, up from 25% today, and natural gas shares range from 18% to 30% of generation, down from 40% today. Coal’s share of generation continues its sharp decline despite changes in policy, for reasons discussed in a recent blog, and nuclear power’s share of total generation slowly declines, although recent announcements by data center providers could change this trend. This analysis shows that the future generation mix will continue to be dominated by renewables and natural gas due to market factors such as technology costs and fuel prices, and that policy changes may affect the rate of growth of each technology but will not be the driving factor in overall deployment.

These scenarios are just the tip of the proverbial iceberg of relevant policy analysis today. Our consultants are uniquely qualified to perform a wide range of energy and environmental scenarios using the NEMS model. The release of the new AEO provides OnLocation with new opportunities to use the latest updated model as the starting point for exploring alternative energy policies and technology advancements to provide insights to our government and private sector clients. For more information about the NEMS model and integrated energy modeling, visit our website and read our NEMS blogs for answers to common questions about the model, including its capabilities and limitations, the cost of a model run, and the time it takes to perform model scenarios.