AEO 2025 Trends: Grid Reliability and Critical Materials

Building Resilience into America’s Energy Future

Grid reliability has emerged as a central energy priority for the current administration, alongside a sharpened focus on securing critical materials. These two goals are increasingly interdependent. Ensuring a stable, responsive, and modern grid depends on technologies, particularly batteries, that in turn depend on strategic materials like graphite and lithium.

This blog is the second in our new weekly OnLocation “AEO25 Trends” blog series. Here we explore how a key piece of energy modeling in the Annual Energy Outlook 2025 (AEO25), utility-scale battery storage, connects directly to the broader national challenge of securing critical materials and ensuring grid reliability.

Utility-Scale Battery Storage: A Case Study in Energy–Materials Interdependence

A key challenge in delivering reliable power in the face of rising demand is maintaining grid stability. Utility-scale battery storage has become a cornerstone solution. These systems provide temporal flexibility by storing electricity during surplus periods and discharging it when demand peaks or generation lags. In this role, batteries serve not just as energy storage, but as critical infrastructure for ensuring grid reliability, enabling operators to balance load, respond to variability, and prevent service disruptions.

This context of growing demand and mounting strain on the grid is inseparable from the challenges in the global supply of materials. On one side, the energy system, especially the electricity sector, is under pressure to expand quickly. Drivers include AI data centers, industrial reshoring, and a broader push for energy dominance. On the other side, materials like graphite, lithium, and rare earth elements are essential to battery technologies and other key energy applications. The global supply chain for these materials, such as battery-grade graphite, is dominated by China. For example, China controls about 80% of global graphite anode production (IEA), and recent export restrictions have only heightened U.S. concerns about supply risks (CSIS). Together, these trends create a direct and urgent need to address grid reliability and critical materials in tandem.

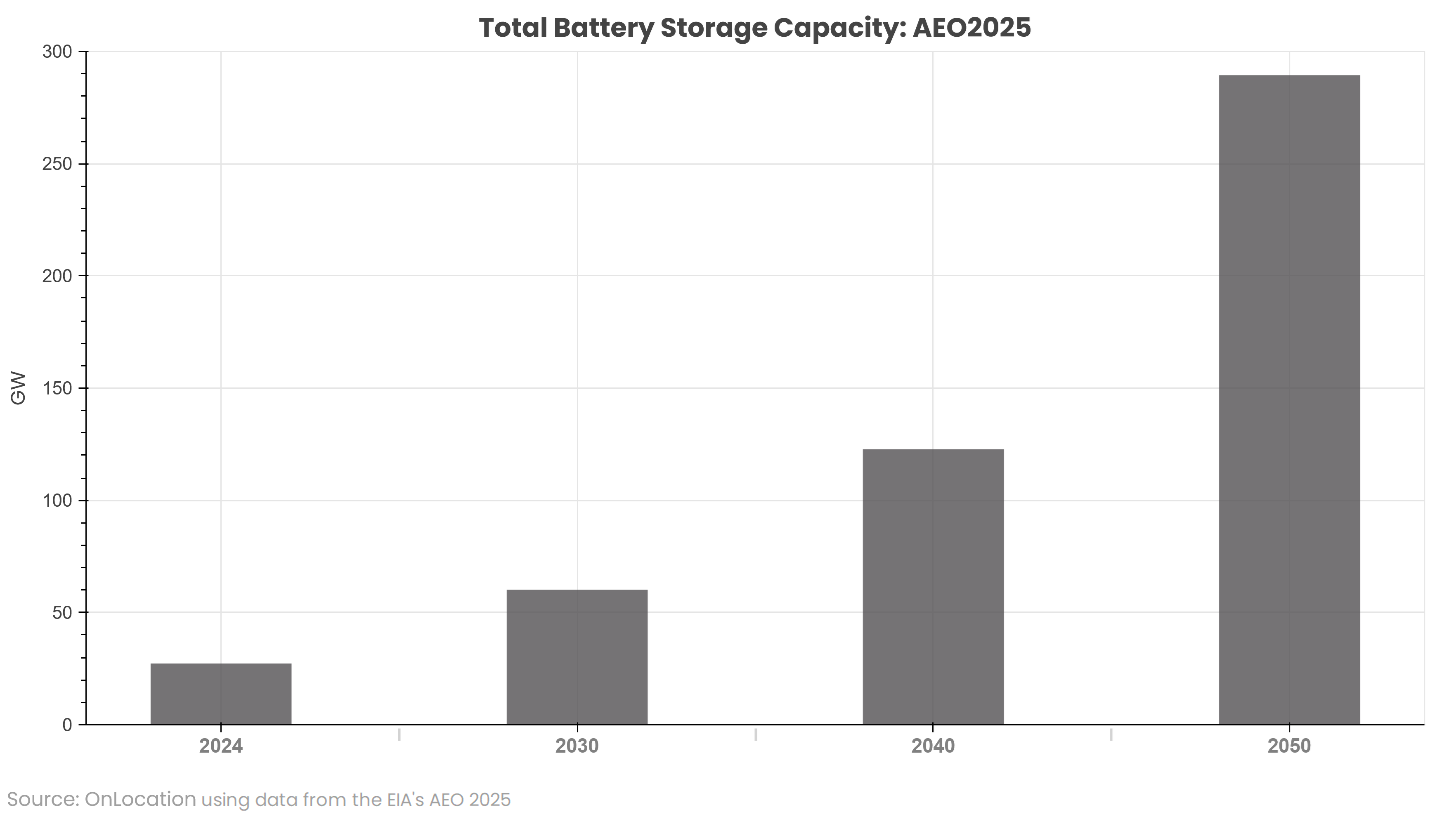

The Annual Energy Outlook 2025 (AEO 2025) Reference case highlights the scale of this trend. The utility-scale battery capacity in the U.S. is projected to grow from 27 GW in 2024 to 289 GW in 2050, a more than tenfold increase. This 262 GW increase reflects a key approach grid operators are planning to accommodate increasingly variable generation and loads.

Figure 1. Battery storage capacity projection in AEO 2025, the Reference case.

This massive buildout raises a key question: what materials will this transition require? The answer depends heavily on battery chemistry. Based on the IEA reports (Minerals, Batteries, Market Review) and the DOE’s 2023 Critical Materials Assessment, a likely scenario could be:

- Lithium Iron Phosphate (LFP) batteries are expected to maintain ~80% market share through 2030.

- Nickel Manganese Cobalt (NMC) batteries will make up most of the remainder.

- By 2050, advanced chemistries like sodium-ion and vanadium-flow batteries could represent up to 35% of the market as they become commercially viable.

Chemistry matters because it defines critical material demand. All the battery types listed here use one or more types of critical materials. While LFP avoids the need for cobalt or nickel, it still uses graphite in its anode. This makes graphite a constant across storage technology pathways.

While this blog focuses on a quick estimate of lithium and graphite demand from utility-scale storage, our team at OnLocation has previously developed a more extensive methodology for analyzing critical materials demand, specifically through our enhancements to NEMS to assess EV deployment. This work demonstrates how material flows can be integrated into system-wide energy modeling.

Using the projected capacity growth from AEO 2025 and technology share assumptions, we estimate cumulative material demand from utility-scale battery storage through 2050 at:

- 81 kilotons of lithium

- 913 kilotons of graphite

To put these figures into perspective, 81 kilotons of lithium is roughly half of the global lithium production in 2023 and approximately equal to Australia’s annual output, the largest producer that year. For graphite, 913 kilotons represent about 57% of global natural graphite production and 75% of China’s annual output in 2023. These comparisons, based on data from the USGS Mineral Commodity Summaries 2024, highlight the scale of projected demand and point to the need for integrating materials considerations into long-term grid planning and investment decisions. This is just one segment of the electricity system. It does not include electric vehicles or solar panels, which also depend on imported material inputs.

Planning for Material Constraints with the Right Tools

As grid infrastructure expands and battery deployment accelerates, materials availability will become a key element of the planning process. Technologies like batteries, wind turbines, and electric motors are physically dependent on global supply chains. That makes energy and material planning inseparable.

Fortunately, we have tools that can help. The National Energy Modeling System (NEMS), which underpins AEO 2025, is well-suited for analyzing critical material needs. The value of deploying NEMS:

- Captures regional and sectoral technological adoption trends over time

- Models technology deployment under alternative policy environments

- Links energy supply, demand, and infrastructure growth

Looking ahead, we plan to implement similar approaches to help assess material needs from solar photovoltaics and wind. We are also considering incorporating materials recycling from consumer electronics or other sources as an approach to increasing domestic supply. As the energy system becomes more complex and interdependent, understanding the role of critical materials will be vital, for federal policy, industrial strategy, and infrastructure investment.

For more insights into the AEO 2025 scenario results, see the recent blogs in our AEO 2025 Trends series including Powering Future Demand as well as our initial AEO 2025 overview blog posted soon after the AEO release in April.